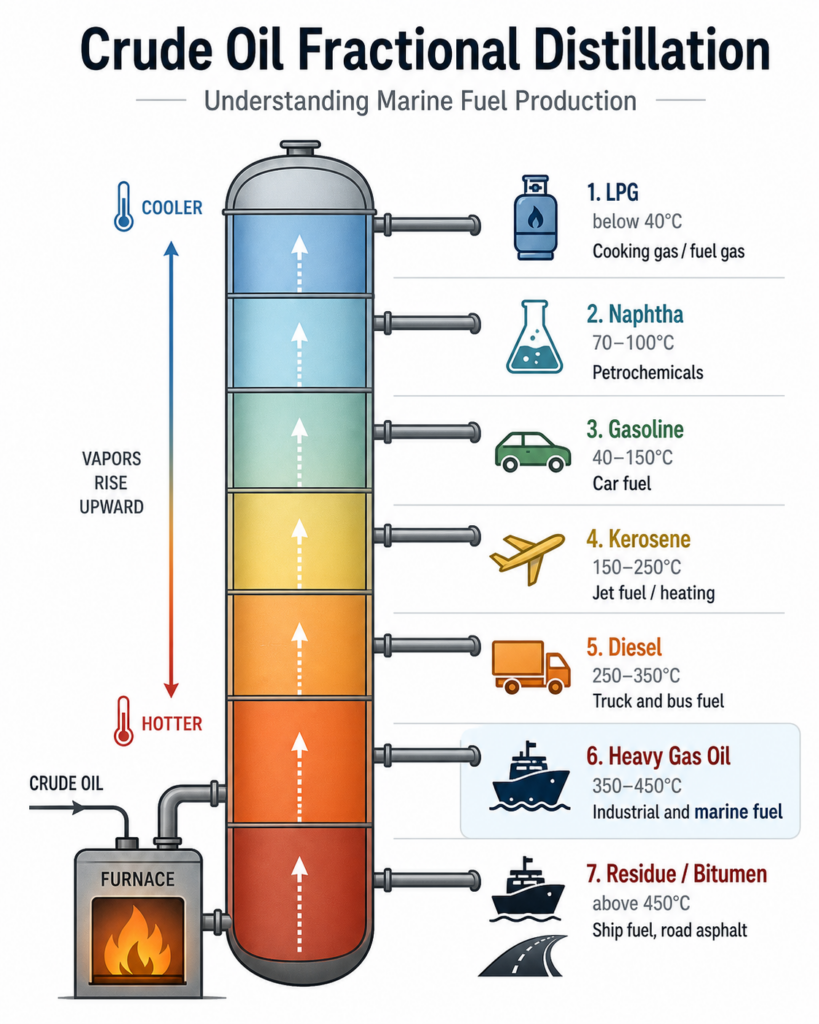

Crude oil is separated through fractional distillation based on boiling points. Lighter products such as LPG, naphtha, and gasoline rise to the top, while heavier products like diesel, fuel oil, and residue remain at the bottom. What looks like a basic chemistry concept is actually the starting point for understanding today’s energy markets.

The U.S. Gulf Coast is now dominated by light crude production, especially from shale. However, the refining system tells a different story. Many large Gulf Coast refineries were originally designed to process heavier crude. Running only light crude creates an imbalance – too much light products like naphtha and gasoline, and not enough middle distillates and heavier outputs.

This is where blending becomes essential.

To optimize yields, refiners mix lighter U.S. crude with heavier crude imported from Canada and Venezuela. But those heavy crudes come with their own constraint – they are too viscous to move efficiently on their own. They require dilution with naphtha or condensate just to be transported.

As a result, a complementary system emerges:

- The U.S. exports light crude and naphtha

- Canada and Venezuela supply heavy crude

This leads to what we call cross-hauling – simultaneous, two-way flows of cargo. Light products move outward, heavy crude moves inward. Shipping demand effectively doubles, routes extend, and ton-mile demand structurally increases.

At the same time, naphtha becomes a critical variable. As more naphtha is diverted into blending and exports, supply tightens in Asia. For petrochemical-heavy economies like Korea, China, and Japan, this directly translates into higher feedstock costs, squeezing margins and pushing product prices higher.

And once prices move up, they tend to stick.

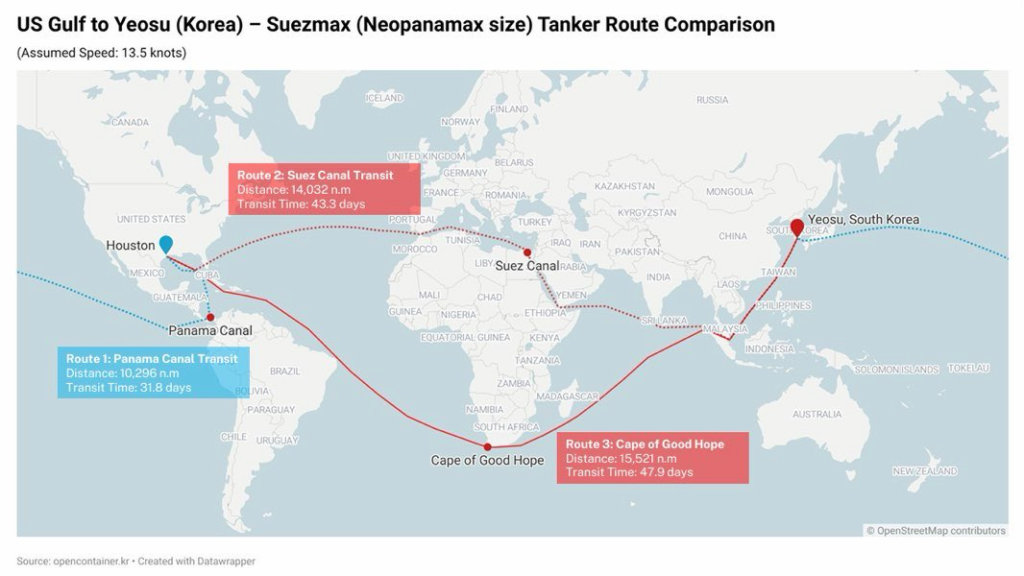

Layer on top of this the rising geopolitical risk in the Middle East. With increased uncertainty around the Strait of Hormuz, some flows are being rerouted. This has contributed to longer voyages and, in some cases, increased utilization of alternative routes such as the Panama Canal.

The result is additional ton-mile expansion – further tightening tanker markets and reinforcing the underlying structural shift.

In the end, today’s energy market is not just about production volumes. It is shaped by:

- the product structure defined by refining

- the necessity of blending

- cross-hauling logistics

- cost pass-through via naphtha

- and geopolitical risk reshaping trade routes

This is no longer a “how much supply” market.

It is a how it’s blended, how it moves, and where it flows market.